Markets Struggle as Oil Prices and Stagflation Concerns Weigh on Stocks

Stocks had another volatile week as the ongoing conflict between the United States and Iran continued to shake global markets.

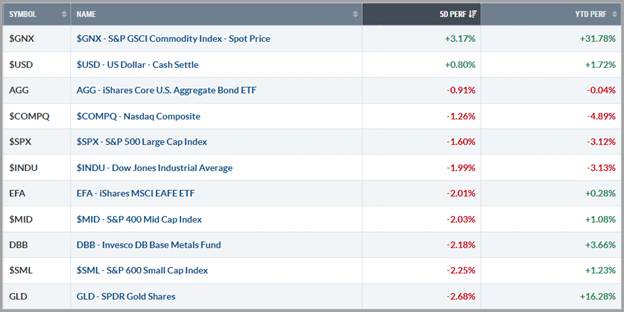

The S&P 500 fell a little more than -1.5% last week and is now down close to 3% for the year.

The biggest driver behind the market’s weakness has been rising oil prices. Escalating attacks around key shipping routes in the Middle East pushed oil briefly above $100 per barrel, which increases concerns about inflation and slows hopes for interest rate cuts.

At the same time, recent economic data has added to concerns about stagflation — a period of slower economic growth combined with stubborn inflation. Fourth-quarter 2025 GDP was revised down to just 0.7%, showing growth is cooling, while the Fed’s preferred inflation gauge (Core PCE) remains around 3.1%, still well above the Federal Reserve’s 2% target.

While the headlines have been dramatic, the market reaction has mostly followed a simple pattern: when oil moves higher, stocks tend to move lower.

The good news is that markets are still holding within their broader trading range, even with the geopolitical tension.

Rates, Dollar & Commodities

Energy markets remain the center of attention. Oil prices surged early in the week, briefly reaching multi-year highs near $120 per barrel after attacks damaged major energy infrastructure in Iran. Prices later cooled but still ended the week higher, with WTI crude rising roughly 9% overall.

The key factor now is the Strait of Hormuz, one of the world’s most important oil shipping routes. If shipping through the region improves, oil prices could fall quickly. If disruptions continue, prices may remain elevated.

The U.S. dollar strengthened, climbing above 100 on the Dollar Index for the first time since late last year as investors looked for stability. Treasury yields also moved higher, with the 10-year Treasury hovering around 4.25%, as higher energy prices raised inflation concerns.

Gold, which had been on a strong run earlier this year, pulled back slightly as rising interest rates and a stronger dollar created pressure.

Takeaway

Right now, three main issues appear to be influencing the market:

- The U.S.–Iran conflict and oil prices

• Concerns in private credit markets

• Ongoing uncertainty around AI investments

The most important one for markets right now is clearly oil prices.

If oil stays above $100 per barrel for an extended period, it could increase inflation and slow economic growth. But if oil falls back toward $80–$90, much of the pressure on stocks could fade.

Aside from energy prices, most economic indicators continue to show stability, though there are signs of emerging weaknesses. Inflation figures last week largely matched expectations yet remain persistently high. While weekly jobless claims are still historically low, the broader outlook suggests a “no hire-no fire” environment, with unemployment gradually increasing but staying at reasonable levels. This week’s GDP report was unexpectedly negative.

That suggests the economy is slowing gradually but not breaking.

This Week – What Matters for Markets

The biggest event this week should be the Federal Reserve meeting on Wednesday.

No one expects the Fed to cut interest rates yet, but investors will be listening closely for clues about when rate cuts might begin.

Earlier this year, markets expected the first cut around June. Because of higher oil prices and inflation concerns, expectations have now shifted closer to September or later.

Investors will also watch several economic reports this week, including:

- Manufacturing data

• Producer Price Index (PPI)

• Weekly jobless claims

Markets will want to see steady growth and stable inflation. Any signs of weakening economic activity or rising inflation could increase volatility.

Broad Overview

The market is currently navigating several uncertainties at once.

Geopolitical tensions, higher energy prices, and questions about future interest rate cuts are all contributing to increased volatility.

Despite that, the broader foundation of the economy still appears relatively solid. Employment remains healthy, inflation is elevated but not spiraling higher, and businesses continue investing in long-term growth areas like technology and artificial intelligence.

Because of that, the current market environment looks more like a period of volatility and adjustment rather than the start of a major downturn.

However, until oil prices stabilize and geopolitical tensions ease, investors should expect continued market swings in the weeks ahead.

If you have any questions about your portfolio or the market outlook, please contact your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.