Weekly Economic Insights

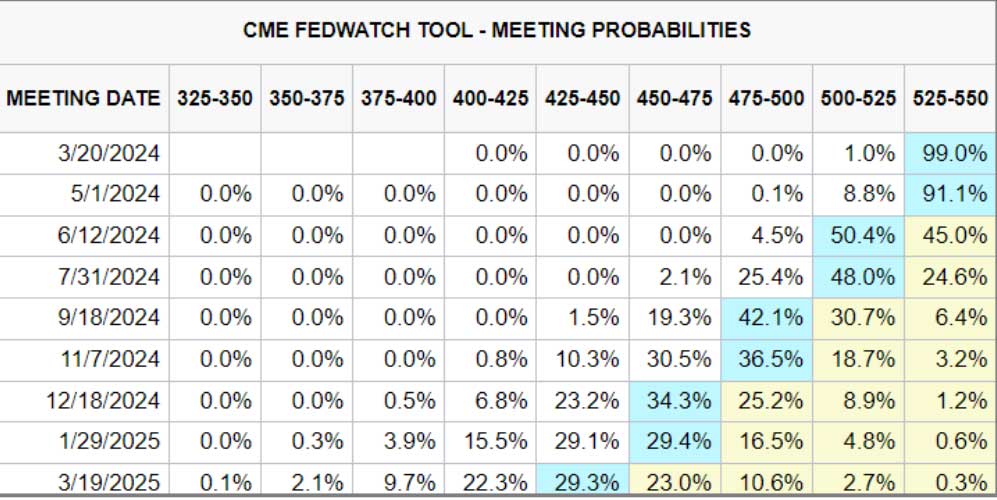

Stocks rallied to new highs early last week before lackluster retail sales, higher-than-expected inflation, and “hot” labor market readings poured a little cold water on the rally. The data points below dampened investor sentiment towards the possibility of a June rate cut, and all but eliminated any hopes for cuts in May as witnessed in the following CME Fedwatch Tool. If upcoming data remains similar, expectations for a June rate cut could decrease further, posing a challenge for both stocks and bonds.

Source: CME Group (https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html)

Producer Price Index (PPI):

PPI surged beyond expectations, indicating higher inflationary pressures than anticipated. This uptick, particularly in core PPI, suggests that inflation might be more persistent than previously thought, raising concerns about future price stability. As PPI influences the Core PCE Price Index, a key inflation measure for the Fed, yields rose following the release.

Consumer Price Index (CPI):

CPI surpassed expectations slightly. However, despite higher-than-expected readings, Core CPI declined year-over-year, indicating a sustained moderation in inflation. Insights from “super core” CPI, suggests that inflation might be moderating more than headline figures imply.

Jobless Claims:

While weekly jobless claims decreased, the context of the hot PPI report intensified their impact on the markets. New claims staying this low suggests a robust labor market and this was further supported by a decline in Continuing Claims. A labor market this strong intensifies the soft landing narrative, but traditionally has a negative impact on the Feds ability to fight inflation.

Retail Sales:

February’s retail sales fell short of expectations, marking the second consecutive month of disappointment. The January data was also revised downward, indicating prolonged weakness in consumer spending.

Key Takeaway:

Although last week’s data was somewhat disappointing as it hinted towards more persistent inflation, it’s important to recognize that these reports are as of one point in time, and do not define a trend in and of themselves. In fact, housing prices have shown a decline which has yet to be factored into the key inflation data points and it’s widely expected that this data, once factored in, will offer even better inflation readings in the future. The current narrative of a soft landing, lower rates in the future, stable employment, and solid economic growth are still the key drivers in this market as evidenced by the S&P reaching all-time highs early in the week. Put simply, it’s going to take a lot more than just a few weak data points to upend current sentiment, but we must keep our eyes on the potential for change.

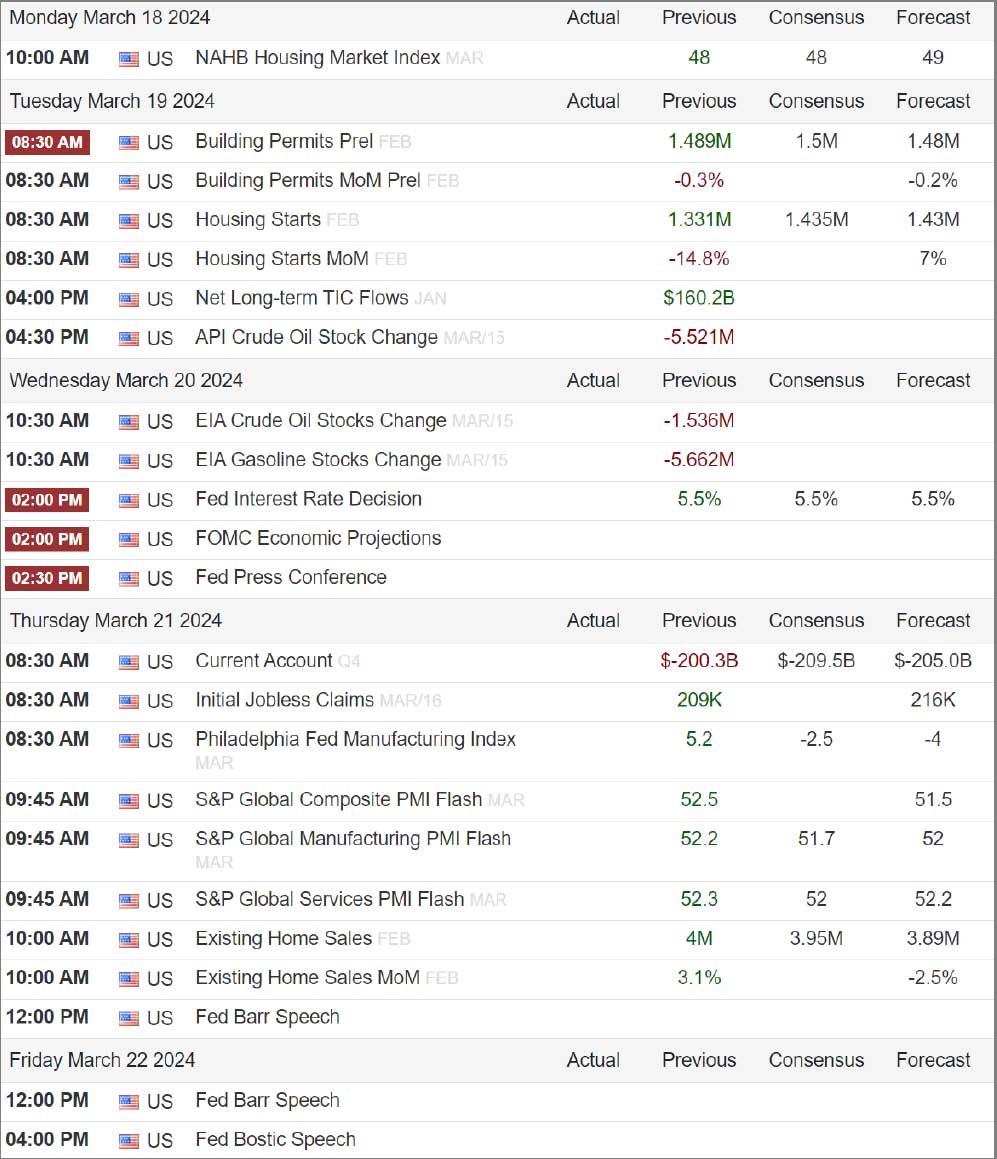

The Week Ahead:

This week’s big event will be Wednesday’s FOMC (Federal Open Market Committee) meeting decision. While you can see in the table above that virtually no one is expecting a rate cut this time around, everyone is interested in the “Dot Plots” (the Fed’s own forward projections). Investors will want to see that three rate cuts remain on the table for 2024. Other notable events are included on the table below with Thursday’s calendar offering some key economic insights with the potential to move markets as well.

Source: Trading Economics (https://tradingeconomics.com/united-states/calendar#)

Tidbits & Technicals:

Headwinds:

- Valuations are frothy given the current rate environment, leaving the markets subject to a potential swift pullback.

- “Higher for Longer”- Risk that the Fed waits too long to begin lowering rates and threatens economic growth.

- Narrow Leadership with just a few mega cap tech stock leading

- Seasonally weak period lasts through the end of March

Tailwinds:

- Optimism surrounding Artificial Intelligence (AI)

- Fed Pivoting from raising rates to potentially cutting in the future.

- Strong Labor Market

- Solid Economic Growth

- Continued Earnings Growth (the pace of which may be slowing)

- Momentum

Sentiment:

- Credit Spreads remain tight, signaling the bond market (aka “Smart Money”) is not worried about a recession in the near future.

- The VIX (CBOE Volatility Index) remains in neutral territory trading with a 14 handle. Note: Periods of low volatility for a long time are often subject to change.

- The CNN FEAR & Greed Index remains above neutral in the “Greed” category showing investors current appetite for risk is strong.

Intermarket Trends:

- The major Indices (Dow Joines Industrial Average, S&P 500, and NASDAQ) have all seen new highs in recent weeks.

- Bond investors have been pricing in the idea of higher for longer recently with 10-year treasury yields flirting with the upper end of this year’s trading range.

- The US Dollar remains right in the middle of its recent trading range.

- Gold has recently made all-time highs.

- Industrial Metals caught a bid recently and copper just broke out of a multi-month trading range.

- Oil is trading near the top of its 2024 range but well below last years highs.

Tying it all together:

Amidst a solid economic backdrop, reasonably strong earnings, and optimism surrounding AI fueling momentum, it’s not surprising the equity markets are within a few points of their all-time highs. For the rally to continue, we’ll want to see a more accommodative Fed stance and we will want to see that sooner rather than later. The bond market is beginning to price in “Higher for Longer” and should that sentiment spill over into the equity markets with valuations this lofty, a swift pullback could occur. I’d view any such pullback as a buying opportunity should the overall economic picture remain bright. Keep in mind that 5-10% pullbacks are very common in the stock market and typically happen a couple times per year. I find the breakout in copper very interesting as this typically signifies renewed economic growth is underway. Coupled with rising Oil (also a key growth metric), low volatility, tight credit spreads and bullish momentum, this market could just do what most bull markets do and surprise investors to the upside.

Please feel free to share these commentaries with friends and family and, should you have any questions regarding your current strategy or the markets in general, please reach out to your CIAS Investment Adviser Representative.

Edward J. Sabo

Chief Investment Officer

Capital Investment Advisory Services, LLC

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.

100 East Six Forks Road; Raleigh, North Carolina 27609

Members FINRA and SIPC