Weekly Market Insights

The past couple of weeks economic data has been generally positive, countering fears of slowing growth which had the markets under a little pressure in late May. The positive news flow began when the May flash PMIs came in notably strong with both manufacturing and services showing significant gains. Jobless claims also stabalized back under the 220k mark, New Orders for Non-Defense Capital Goods ex-Aircraft (NDCGXA) showed business spending plateauing but not declining while the revised Q1 GDP showed solid growth at 1.3%. From an economic activity perspective, this was all “good news”. Last week, the Core PCE Price Index met expectations at a 2.8% year-over-year increase, easing investor concerns about inflation and not altering expectations for Fed rate cuts.

Key Takeaway:

The past two weeks’ data has been generally positive. Although yields rallied on the positive data as investors initially priced in the “Higher for Longer” interest rate narrative and pressured stocks, Friday’s Core PCE (the Federal Reserves preferred inflation metric) seems to have calmed investors nerves.

The Week Ahead:

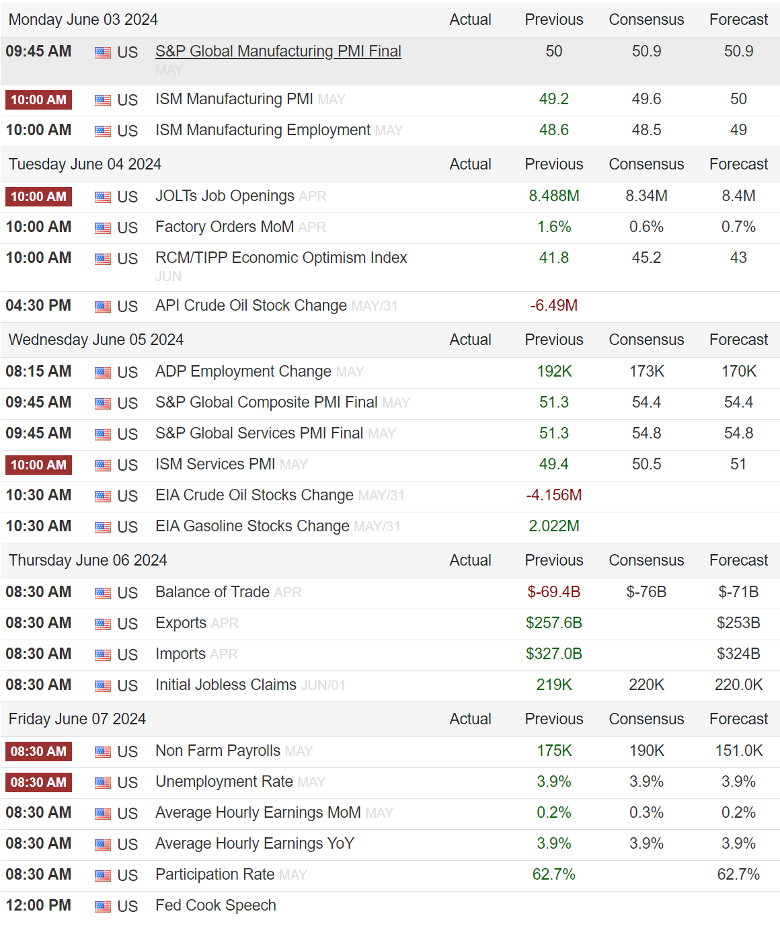

Once again, it’s Jobs week, but before we get to Friday’s all-important employment reports, we will see ISM Manufacturing PMI today and the ISM Services PMI on Wednesday.

Once again, investors will cheer “Goldilocks” data (not too hot, not too cold) as that will keep the 2-rate cut thesis for this year on the table without destroying growth. In this fickle market, soft data has been received rather well of late, so one would expect lower rates and a rally in equities so long as the data isn’t too strong.

Source: Trading Economics (https://tradingeconomics.com/united-states/calendar#)

Tidbits & Technicals: (New developments will be denoted via***)

Current Headwinds:

- ***Valuations seem frothy given the current rate environment, leaving the markets subject to a potential swift pullback!

- “Higher for Longer” – Risk that the Federal Reserve waits too long to begin lowering rates and threatens economic growth.

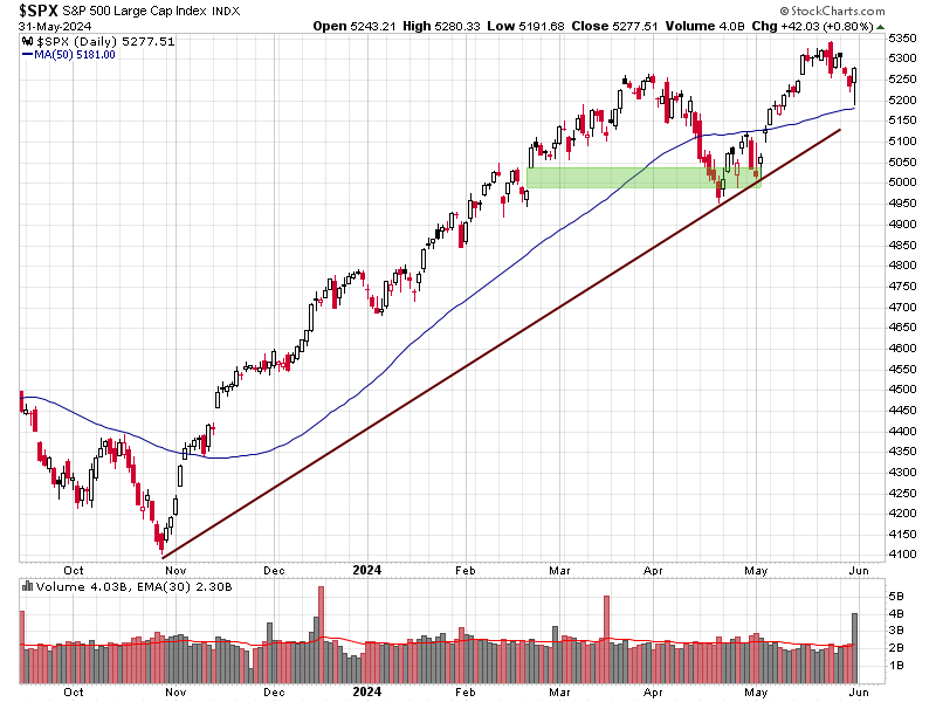

- 10-year Treasury yields recently broke out to new highs for the year signaling that bond investors may be beginning to believe in the “Higher for Longer” thesis but have retreated more than 25 basis points (.25%) in May

Current Tailwinds:

- Optimism surrounding Artificial Intelligence (AI)

- Federal Reserve pivoting from raising rates to potentially cutting in the future.

- Strong Labor Market

- Solid Economic Growth

- Continued Earnings Growth (the pace of which may be slowing)

- Momentum

- Participation is broadening with cyclicals taking a leadership role while the tech-trade begins to fade.

Sentiment:

- Credit Spreads remain tight, hitting their lowest levels recently since peaking in 2022 signaling the bond market (aka “Smart Money”) is not worried about a recession in the near future.

- The VIX (CBOE Volatility Index) is back to the lower levels of the complacency zone.

- ***The CNN FEAR & Greed Index has returned to Neutral signifying a balanced sense of investor optimism.

Intermarket Trends:

- The major Indices (Dow Jones Industrial Average, S&P 500, and NASDAQ) recently posted new highs signifying a positive trend.

- ***Interest rates crept back up recently as investors perceived the recent bout of strong economic data to keep rates higher for longer. Rates were somewhat cooled by last week’s inline Core PCE but remain volatile.

- The US Dollar is trading near the upper end of this year’s trading range due to foreign central banks being the first to cut rates and others taking further rate hikes off the table while the Fed continues its campaign of tough rhetoric.

- Gold is trading near record highs.

- Industrial Metals raced higher recently and copper recently broke out of a multi-month trading range.

- Oil futures have pulled back from recent highs and are trading in the middle of their one-year trading band.

Tying it all together:

The economy and the market are stable for now. Four factors have driven the market since October: strong growth, falling inflation, expectations of Fed rate cuts, and tech stock strength. These factors remain intact despite some of the alarming headlines that have surfaced a few weeks ago.

In April, stocks fell when it seemed the Fed might not cut rates in 2024. Now, markets expect two rate cuts in 2024, starting in September. Coming into the year I heard expectations for seven rate cuts… These shifts could cause short-term volatility, but we’re not generally focused on the short term. Whether the Fed cuts rates in September or December isn’t crucial, as long as a cut is coming. If the market drops soon due to rate-cut worries, it’s likely a buying opportunity rather than a long-term problem.

In the long term, the key concern is economic growth. It’s strong now, but we need to watch for signs of a slowdown, as that could be detrimental to the markets. High interest rates aren’t as much of a major concern so long as growth remains solid.

For now, this is all “to be watched” as the positives (full employment, declining inflation, economic growth, strong earnings, etc.) currently far outweigh the negatives and until those change, conditions are favorable for risk assets. Environments like this have best been navigated in the past by making certain one’s overall portfolio is in line with their risk tolerance and focused on achieving long term goals.

Please feel free to share these commentaries with friends and family and, should you have any questions regarding your current strategy or the markets in general, please reach out to your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.

100 East Six Forks Road; Raleigh, North Carolina 27609

Members FINRA and SIPC