Markets Edge Higher After Early Surge Fades

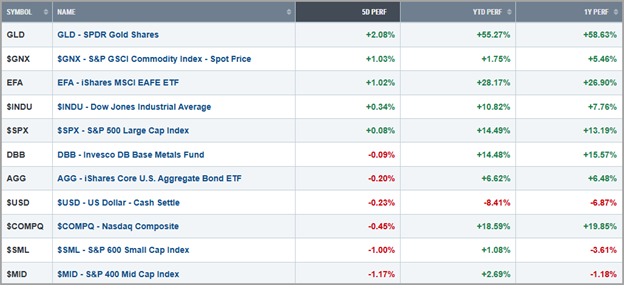

U.S. stocks jumped early last week after a deal to end the government shutdown sparked a broad risk-on move, especially in beaten-down tech stocks. But concerns about stretched valuations and rising uncertainty around what the recently delayed economic data may reveal (particularly on the labor market and consumer spending) gradually erased most of those gains. The S&P 500 ended the week nearly flat while the NASDAQ slipped just under 0.5%. Smaller stocks were down around 1%.

The early optimism was tempered by renewed skepticism toward AI valuations, disappointing guidance from several AI-linked firms, and lingering concerns about global growth, especially after evidence of a weakening Chinese economy and cautionary comments from the International Monetary Fund about “mounting strain” in the U.S. Adding to the unease, the Bureau of Labor Statistics announced that the long-delayed September jobs report will not be released until November 20, keeping investors in the dark about a key pillar of the outlook.

Still, despite pockets of volatility and a meaningful mid-week pullback, dip buyers defended key technical levels, helping markets stabilize into the weekend.

Rates, Dollar & Commodities

Treasury yields were steady, with the 10-year holding just above 4.10% as mixed labor data and shifting Fed expectations kept rates in a neutral range. The U.S. dollar slipped 0.25%, weighed down by a soft ADP report that modestly lifted odds of a December rate cut while commodities saw moderate swings as markets adjusted to the reopening of the government and uncertainty surrounding U.S. data.

Oil whipsawed on geopolitical news but recovered late in the week to finish up just under $60/barrel, and Gold surged toward $4,250 on safe-haven demand before retreating on some rather hawkish (keeping rates unchanged) Fed commentary. Copper rose nearly 2%, a modestly constructive macro growth signal despite the economic concerns over in China.

Takeaway

Markets continue to grapple with a familiar mix of themes: elevated valuations, divergent signals around AI-driven growth, and growing concern about what delayed economic data may reveal. Last week’s swings highlighted a cautious tone as investors balance strong year-to-date gains against lingering macro uncertainty.

Still, technical support (where traders expect prices to stall or change direction based on past moves) largely held, risk appetite remained intact beneath the surface, and expectations for eventual policy easing helped limit downside. For now, the recent volatility appears to be a normal consolidation phase—not a signal of a broader trend reversal.

Source: stockcharts.com

Looking Ahead

With government data still delayed, markets will focus mostly on this week’s private-sector data once again. The key release is Friday’s flash composite PMI, the first national read on November activity. Prior to that, Empire State and Philly Fed surveys will offer initial snapshots of November conditions. While less influential than the PMIs as these are survey-related and often volatile, a sudden drop in either would raise concerns about weakening momentum. Tuesday’s ADP jobs report also matters after last week’s soft reading. A rebound would calm labor-market worries; another decline would do the opposite.

Finally, the FOMC minutes will give insight into how much support exists for a potential December rate cut. Signs the Fed remains open to further easing would be market-friendly, while evidence of deeper division could pressure sentiment.

Broad Overview

Markets are juggling a mix of encouraging and concerning signals, though overall optimism remains. Investors continue to draw confidence from strong consumer demand, steady corporate spending on artificial intelligence, and expectations that the Federal Reserve will eventually begin lowering interest rates. Inflation has eased significantly since 2022, and the job market is cooling gradually, both suggesting the economy could achieve a “soft landing” rather than slipping into recession.

Still, several warning signs are emerging. Borrowing costs are creeping higher, the strong U.S. dollar threatens to weigh on company profits, and a narrower group of stocks continues to drive most of the market’s gains — conditions that have historically preceded short-term pullbacks. Adding to the caution, investors are starting to question the sustainability of AI “circular financing”, a practice in which big tech firms invest (or commit to investing) in AI projects with other companies and then spend heavily on those same firms’ services. While it boosts revenues on paper, this loop can mask how much real, organic demand for AI products actually exists and begs the question, “Who is really paying the bill for all this expenditure?”

The bond market, often a reliable gauge of economic expectations, continues to signal a slow and steady cooling rather than a sharp downturn. As November unfolds (a month that historically favors equities) market strength may stay concentrated in a few large-cap names before broader participation returns. The key question now is whether investor optimism can endure as valuations stretch higher and the Fed’s tone remains cautious.

We’ll continue to watch these trends closely and keep you updated. If you have any questions about your portfolio or the markets, please contact your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.