Markets Bounce Back After Early Week Lows

Last week started a bit shaky for stocks, but the market recovered nicely by the end of the week. Investors were watching several things at once such as AI investment concerns, economic data, and global headlines, but overall, conditions ended up supportive.

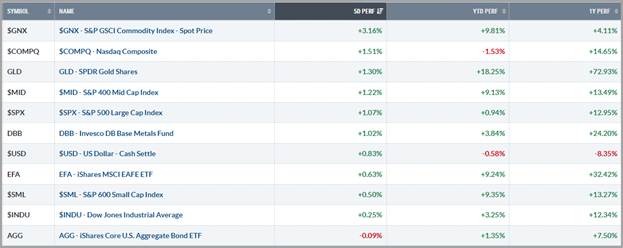

The S&P 500 finished the week up a little more than 1% and is now in positive territory for the year.

One reason markets steadied was that fears around AI disruption cooled a bit. At the same time, economic data came in what many call “Goldilocks”- strong enough to show the economy is growing, but not so strong that it pushes interest rates sharply higher.

There was also plenty of news around tariffs and global tensions, but nothing escalated enough to cause lasting damage to markets. By the end of the week, investors were stepping back in and buying stocks again.

The big picture? The market dipped early, but buyers showed up and pushed things back higher.

Rates, Dollar & Commodities

Interest rates moved slightly higher during the week, with the 10-year Treasury yield ending just under 4.10% while the U.S. dollar strengthened as economic data showed solid growth and inflation remained somewhat elevated. A stronger dollar can sometimes slow markets, but movements were fairly orderly.

Commodities had a strong week overall as oil reached a six-month high, helped by stronger economic data and ongoing tensions in the Middle East. Precious metals also gained, with gold hitting new February highs as investors continued to use it as a safety hedge.

Meanwhile, industrial metals like copper also rose, showing optimism about economic activity and future demand tied to technology and infrastructure.

Overall, commodities showed broad strength last week.

Takeaway

If there’s one theme right now, it’s that the market is still moving forward, even with uncertainty.

There are ongoing concerns about AI investments, inflation, and policy decisions, but the overall economy has continued to show steady growth.

Recent economic reports show that businesses are still investing, manufacturing activity is expanding, and the labor market remains stable. Inflation is still somewhat elevated, though, which means the Federal Reserve may take its time lowering interest rates.

In simple terms: the economy is strong, but not perfect — and that’s keeping markets a bit volatile.

This Week – What Matters for Markets

This week, investors will be watching a few key things.

Focus this week will be on housing and producer price data, which can influence inflation readings. If home prices remain stable, that would historically be a positive sign for inflation trends.

Weekly jobless claims remain an important data point but the biggest attention this week may actually be on major technology earnings, especially companies tied to AI. Strong results could help calm recent concerns around the tech sector and support the broader market.

Broad Overview

Right now, the market feels like it’s going through a period of adjustment rather than a downturn.

Stocks are reacting to a mix of factors — AI expectations, inflation trends, interest rates, and global politics. That can create short-term swings, but underneath it all the economy continues to grow.

Consumer spending remains steady, businesses are still investing, and many sectors outside of technology are performing well.

As long as those trends continue, the overall outlook for the market remains constructive, even if volatility sticks around.

If you have any questions about your portfolio or the market outlook, please contact your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.