Markets Rally Again—Momentum Builds

Stocks wrapped up last week on a strong note, notching gains the second week in a row. The S&P has now risen for nine straight trading days—its longest winning streak in over 20 years.

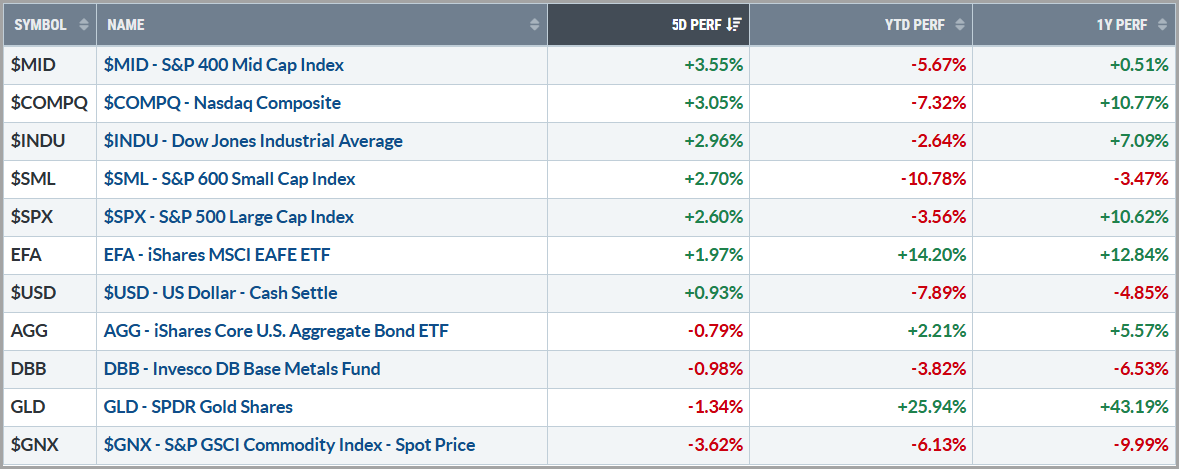

What’s more, the steep selloff following the April 2 tariff announcement has been fully reversed for the S&P 500 and Nasdaq, with both benchmarks now comfortably above those levels. While the Dow, small-cap Russell 2000, and mid-cap S&P 400 still have ground to recover, all are up double digits from their early April lows.

China announced tariff exemptions on roughly 25% of U.S. imports just days after the U.S. offered exemptions on numerous tech-related items, demonstrating that negotiations are under way despite the fact both parties officially state that no talks are taking place at this time. Adding to the excitement, Friday’s Employment Report beat expectations, with the U.S. adding 177,000 jobs in April, well above forecasts despite other labor market reports throughout the week having missed expectations.

Outside of labor, key economic reports largely missed expectations with Q1 GDP contracting for the first time in three years, while Consumer Confidence hit its lowest level since 2011! Yes, lower than witnessed during the COVID Pandemic. Inflation expectations rose significantly as well, although Core PCE, the Federal Reserve’s preferred inflation gauge, met expectations. Earnings for the week came in good with surprise beats by tech giants Meta (Facebook) and Microsoft.

When all was said and done, yields were up across the curve with 10-year treasuries closing out the week just .05% higher, near 4.31%. The dollar was also little changed, but commodities in general traded down.

Source: stockcharts.com

The Week Ahead:

This week’s economic calendar will feature the ISM Services report and Wednesday’s FOMC interest rate decision meeting. While very few expect the Fed to cut rates this week, everyone wants to hear their thoughts regarding what’s going to come in the future. Regarding the ISM Services PMI, a strong number is getting more and more important to negate the slowdown rhetoric of late. Any significant miss could reignite stagflation fears and increase market downside risk significantly.

Tying it all together:

Uncertainty has been driving the markets lately, as investors seemingly fear that the new administration’s tariff policies and potential trade wars could induce a recession, despite the fact that hard economic data remains largely firm. The S&P 500 technically entered “Bear Market” territory, having slid over -20% from its recent highs before rebounding, and the new intermediate trend direction needs to be respected.

So far, defensive sectors, value stocks, and low-volatility names have held up relatively well. At the same time, maintaining diversification and strategically overweighting safe havens like bonds and precious metals, has provided added comfort to stay the course. We are certainly not out of the woods just yet, but a glimmer of hope has emerged as some of the economically-sensitive assets like commodities have begun to trade up, the dollar has weakened a good bit, which may provide a tailwind to corporate profits, and tariff negotiations are underway. Markets are functioning properly with plenty of liquidity and the bond market, aka “Smart Money”, appears to have calmed down for now.

How this will all play out is yet to be seen, but please keep in mind that market downturns, such as the current one, have historically presented opportunities for long-term investors. These periods may allow for acquiring assets at more favorable valuations and securing stronger portfolio yields. It’s important to maintain a long-term perspective while exercising patience, vigilance, and diversification. Historically, these market conditions have tended to be short-lived, often rewarding those who remain focused on their long-term investment goals.

Please feel free to share these commentaries and, should you have any questions regarding your current strategy or the markets in general, please reach out to your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.

100 East Six Forks Road; Raleigh, North Carolina 27609

Members FINRA and SIPC