Weekly Market Insights

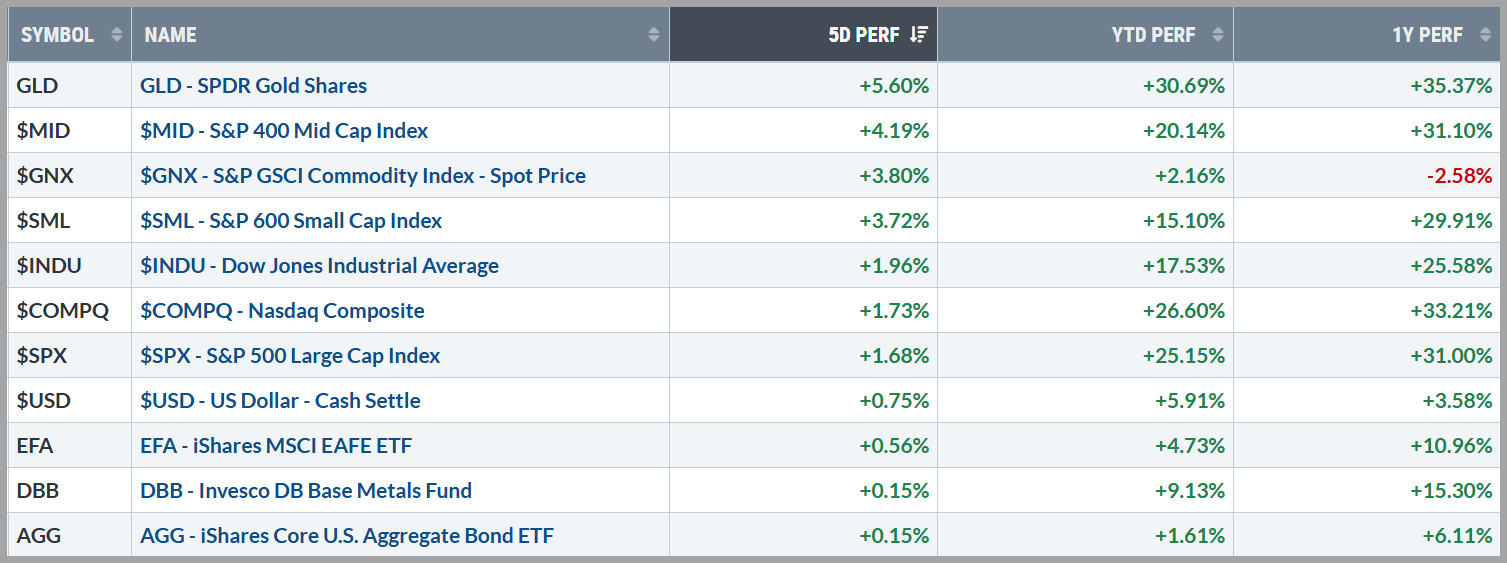

Investors embraced last week’s “Goldilocks” economic data (solid growth that doesn’t hinder hopes for future rate cuts) along with more traditional Presidential Cabinet appointees (ones that will promote pro-growth policies, such as tax cuts and deregulation, while pushing back on some of the more radical ideas that could be inflationary, like widespread tariffs). When all was said and done, the major stock indices posted strong weekly gains led by small-cap and mid-caps up around 4%, while the larger indices were all north of 1.5%.

Treasury yields were largely unchanged last week with the 10-year yield hovering around the 4.40% mark, despite the solid economic growth data in the US while the dollar spiked to new highs for the year amid weaker European data. Commodities rallied across the board led by advances in Oil and Gold thanks to intensified geopolitical unrest as Ukraine sent US-made missiles into Russian territory — a move Russia warned would have consequences.

Source: Stockcharts.com

Key Takeaway:

Solid economic data, coupled with hopes for future rate cuts and a pro-growth political agenda, are driving investor optimism despite relatively high valuations. Nvidia, the largest company by valuation and “most important” tech stock in the world right now, once again posted solid, near triple digit growth and forward guidance, keeping the AI theme alive. Many of the key retailers also posted solid results last week, demonstrating the consumer is still spending. The path of least resistance for stocks appears to be higher and sentiment is strong. We will be keeping a close eye on longer-term interest rates, as any signs of higher for longer could pour some cold water on this hot market, but for now, a Santa Clause Rally is looking promising to close out the year.

Source: Optuma with DTN IQ data

The Week Ahead:

With markets closed Thursday and a half day Friday for Thanksgiving, key economic data will be concentrated on Tuesday and Wednesday. While the critical monthly reports aren’t due till next week, this week’s readings could still influence markets.

On Wednesday, notable releases include the revised Q3 GDP, October Durable Goods, and the Core PCE Price Index—the Fed’s preferred inflation measure and the most important of the three. Additionally, the Fed’s November meeting minutes will be released Tuesday, offering potential clues on future rate cuts. Any indication of hesitation on rate cuts could weigh on markets, while confirmation of a consensus for continued cuts would be positive.

Current Observations

Economic Growth: The economy appears to be growing at a moderate pace, not too hot. GDP expanded 2.7% year-on-year in the third quarter of 2024, slowing slightly from a 3% rise in the previous period and has averaged 3.16 percent from 1948 until 2024.

(source: U.S. Bureau of Economic Analysis)

Inflation: Inflation has been cooling over the past year but appears to be a little “sticky” in recent months. The annual inflation rate in the US accelerated to 2.6% in October 2024, up from 2.4% in September which was the lowest rate since February 2021. This marks the first increase in inflation in seven months while core consumer prices, which exclude volatile items such as food and energy, remain unchanged from September.

( source: U.S. Bureau of Labor Statistics)

Employment: The jobs market remains robust despite the recent rise in unemployment from historically low levels and the decreasing number of job openings. Put simply, the labor market was on fire just a few months ago and is cooling off to sustainable levels. The unemployment rate in the United States fell to 4.1% in September 2024, the lowest in three months, down from 4.2% in the previous month.

(source: U.S. Bureau of Labor Statistics)

Monetary Policy: The Fed lowered the federal funds target range by 25 basis points to 4.5%-4.75% at its November 2024 meeting, following a jumbo 50 basis point cut in September in an effort to balance inflation confidence with labor market concerns. An effective fed Funds Rate of 4.625% is still considered “restrictive policy”, yet the fed has telegraphed this is only the beginning of a rate cut cycle.

(source: Federal Reserve)

Sentiment: Investor psychology is presently bullish. According to AAII, retail investor Bulls currently outweigh the Bears by a decent margin, approaching euphoric levels despite the recent pullback. Active money managers appear to be near fully invested in stocks with the NAAIM Exposure index exceeding the 90% level while the CNN Fear & Greed index, which measures seven different aspects of market behavior to gauge the “mood” of the stock market, is in “Greed” territory.

Volatility & Speculative Demand: The VIX (CBOE Volatility Index), which is known to be Wall Street’s Fear Gauge, remains “Complacent” following election week. This falls in line with what Yield Spreads, the difference (or spread) between yields for junk bonds and safer government bonds, have been signaling all year – as they are at historical lows – a sign that investors may be willing to take on more risk with regards to their fixed income investments and confidence in the overall economy.

Stocks

The major Indices (Dow Jones Industrial Average, S&P 500, and NASDAQ) near all-time highs signifying a positive trend. Outside of the US, Developed and Emerging Markets Indices, which peaked in late September, have spent the last month retreating with their currency hedged counterparts holding up much better.

Bonds & Interest Rates

Bonds have had a relatively rough time since the Fed cut rates in September. A wave of overwhelmingly positive economic data and governmental policy concerns have rekindled inflation fears, causing investors to recalibrate their upcoming rate cut expectations. (Just a reminder, bond prices and interest rates have an inverse relationship)

Commodities & Currencies

The weak Chinese economy (2nd largest in the world) and strong US dollar continue to weigh on commodities. Oil, the largest component in the commodities space, along with industrial metals (a key global growth gauge), have been under pressure while precious metals are trading near all-time highs.

The US Federal Reserve is currently being viewed as the most “Hawkish” (high rates) central bank in the world. This stance is keeping a bid under the US Dollar as it trades near cycle highs.

Breadth & Technicals

One of the major themes since the markets sold off in August has been expanding breadth. More and more stocks have joined the parade to higher prices and that’s a good thing. Recent economic data supports this breadth expansion to the more cyclical areas of the market while the overall trend towards economic expansion and lower interest rates is supporting the cyclical trade.

Advancing stocks have been outpacing decliners for the past several months while the pace of net new 52-week highs continues to expand. This positive momentum is also shadowed by a healthy reading of stocks with a Point & Figure “buy” rating (an objective measure of bullish price patterns and demand).

Tying it all together:

Stock market momentum remains strong, and for good reason. Inflation is gradually cooling, and interest rate cuts are providing a boost, while economic growth is robust, and the job market is showing steady resilience. On top of that, corporate earnings projections are climbing.

It looks like the Fed’s strategy to guide the economy toward a “soft landing”, a scenario where an economy slows down just enough to curb inflation without falling into a recession, seems to be bearing fruit, and the market is reacting positively.

The primary driver behind the stock market rally is the seemingly prevailing belief that the economy will avoid a severe downturn, achieving a soft landing instead, which, combined with potential Fed rate cuts, could create an ideal “Goldilocks” scenario for stocks. However, it’s crucial to remain cautious, as challenges persist, and current valuations appear somewhat “frothy.”

Encouragingly, investor sentiment is optimistic, but not yet euphoric, and stock price gains are now extending beyond just the technology sector. Broad sector participation is a positive sign for sustained market growth, and we are seeing this at a time when historically significant seasonal patterns are coming into play. The old adage, “Sell in May and go away” [until October], is ringing in the ears of Wall Street participants as we enter the traditionally “strong” season of November-through-April.

Volatility has been pronounced in the bond market this year, with long-term interest rates showing some of the most significant fluctuations in decades. The 10-year Treasury yield hit a peak of around 5% last October, started the year in the upper 3% range, rallied back to approximately 4.75% around May, and has since returned close to where it began this year. Meanwhile, short-term rates have remained more stable, aligning more closely with Federal Reserve policy and showing signs of easing as the first rate cuts have taken effect. Recently, a shift has occurred in the yield curve: for the first time since mid-2022, long-term Treasury yields (10-year) exceeded short-term rates (2-year), breaking a historic inversion that lasted 783 days.

With the first rate cuts now implemented, it seems that the economic disruptions triggered by the COVID outbreak and governmental stimulus efforts—such as inflation, workforce challenges, and supply chain issues—are receding into the past. The primary focus has shifted back to future growth, earnings, employment, and innovation, signaling a potential return to “normal” in the markets, if such a state is indeed achievable.

Please feel free to share these commentaries with friends and family and, should you have any questions regarding your current strategy or the markets in general, please reach out to your CIAS Investment Adviser Representative.

Important Disclosures:

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The statements contained herein are solely based upon the opinions of Edward J. Sabo and the data available at the time of publication of this report, and there is no assurance that any predicted or implied results will actually occur. Information was obtained from third-party sources, which are believed to be reliable, but are not guaranteed as to their accuracy or completeness.

The actual characteristics with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account; (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment. Capital Investment Advisory Services, LLC (CIAS) reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. The information provided in this report should not be considered a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time you receive this report or that securities sold have not been repurchased. The securities discussed may not represent an account’s entire portfolio and in the aggregate may represent only a small percentage of an account’s portfolio holdings. It should not be assumed that any of the securities transactions, holdings or sectors discussed were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

CIAS is a registered investment advisor. More information about the advisor, including its investment strategies and objectives, can be obtained by visiting www.capital-invest.com. A copy of CIAS’s disclosure statement (Part 2 of Form ADV) is available, without charge, upon request. Our Form ADV contains information regarding our Firm’s business practices and the backgrounds of our key personnel. Please contact us at (919) 831-2370 if you would like to receive this information.

Capital Investment Advisory Services, LLC

100 E. Six Forks Road, Ste. 200; Raleigh, North Carolina 27609

Securities offered through Capital Investment Group, Inc. & Capital Investment Brokerage, Inc.

100 East Six Forks Road; Raleigh, North Carolina 27609

Members FINRA and SIPC